In modern enterprise management, "Credit First" is becoming a common choice for teams pursuing extreme efficiency. Distributing corporate credit cards (like Mercury Cards) to employees and allowing them to "spend first, reconcile later" without tedious prior approvals significantly boosts the business team's agility.

However, for finance teams, this convenience often means a nightmare: dozens or hundreds of transaction records pouring in daily, each requiring manual verification, expense attribute judgment, account classification, and individual system entry.

How can we maintain the flexibility of "Credit First" without burying Finance in repetitive labor?

As a technology-driven organization, the Dify team faced the exact same dilemma. Today, from the perspective of CIOs and Finance Managers, we want to share how we used Dify Workflow to transform this complex financial process into "auditable intelligent automation."

The Real Financial Dilemma: It Looks Like Entry, But It's Actually Judgment

Outsiders often think finance work is just "organizing data," believing a simple API integration can solve it. But the real pain point is not data movement, but judgment.

Behind every seemingly simple transaction lies complex business logic:

- Supplier Ambiguity: The same AWS bill could be R&D expenses last month, prepaid cloud resources this month, and cross-departmental allocation next month.

- Rule Lag: New suppliers emerge endlessly, and carefully maintained rule tables are always one step slower than business changes.

- Error Amplification: A single mistake isn't just one correction; the subsequent tracking, explanation, and audit sampling amplify the cost of this error several times over.

Traditional automation (RPA, rule engines) is efficient at "moving data," but becomes helpless once it encounters scenarios requiring "reading notes, combining history, and then categorizing."

We need an "Intelligent Assistant" that can understand business context and exercise judgment, yet strictly abide by financial discipline.

Why Choose Dify Workflow?

When selecting technology, managers often face a choice: fully autonomous AI Agents or structured Workflows?

In financial automation, where explainability, reviewability, and auditability are required, our experience suggests agentic workflows are typically the most reliable approach.

Agent vs. Workflow: Self-Driving Car or High-Speed Rail?

- Agent is like a Self-Driving Car: Give it a destination, and it plans its own route. This is flexible, but in financial scenarios, it means uncontrollable, hard to review, and hard to audit.

- Agentic Workflow is like a High-Speed Rail: The tracks are laid in advance (critical processes are fixed), and the train only makes choices at limited junctions (intelligent judgment is introduced only at a few nodes).

Financial automation allows for zero deviation. It must be as rigorous and reliable as a high-speed rail, while possessing enough flexibility to handle complex scenarios. The core value of Dify Workflow lies precisely in allowing us to build a rigorous rule framework while embedding LLM cognitive capabilities at critical nodes.

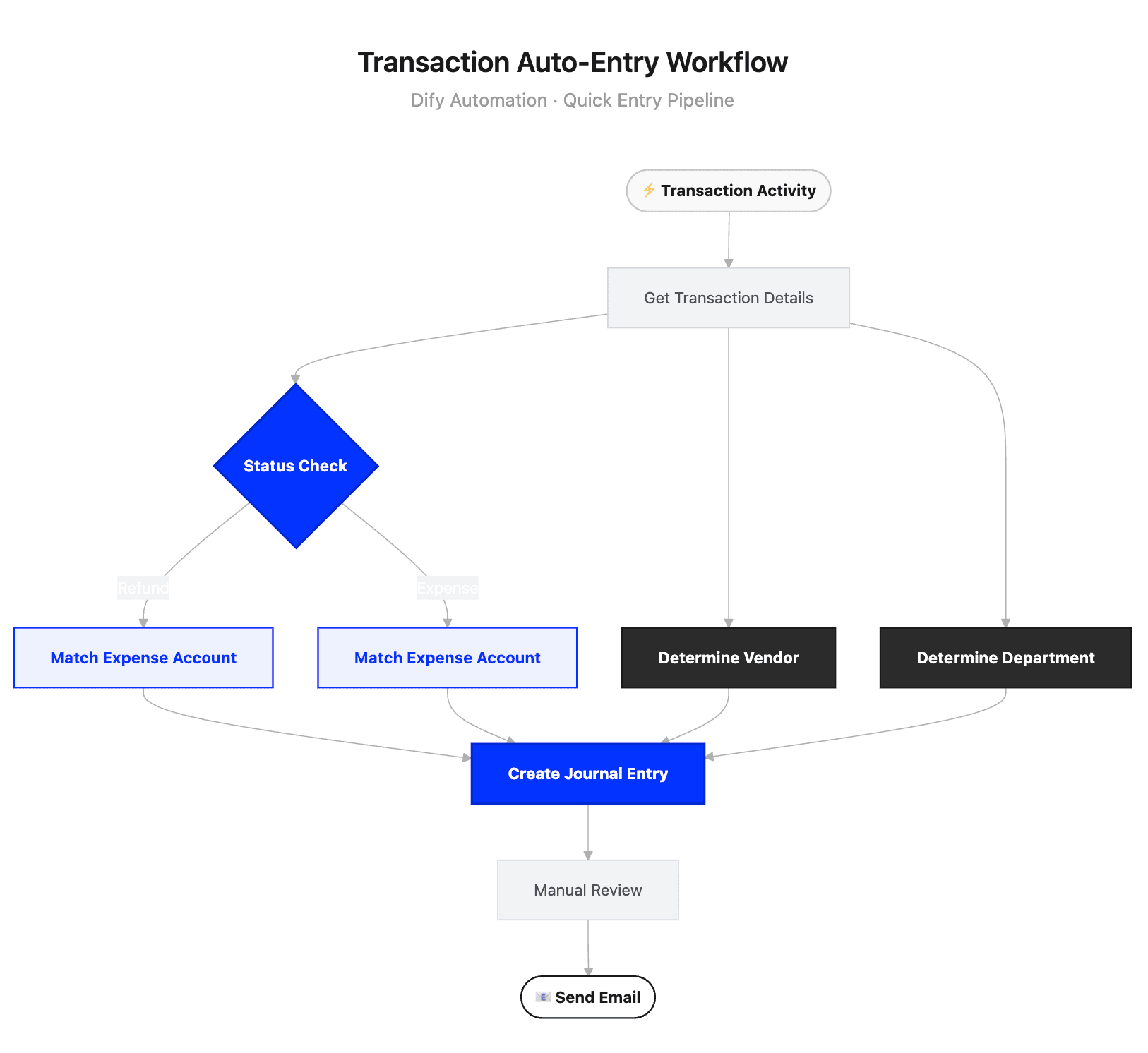

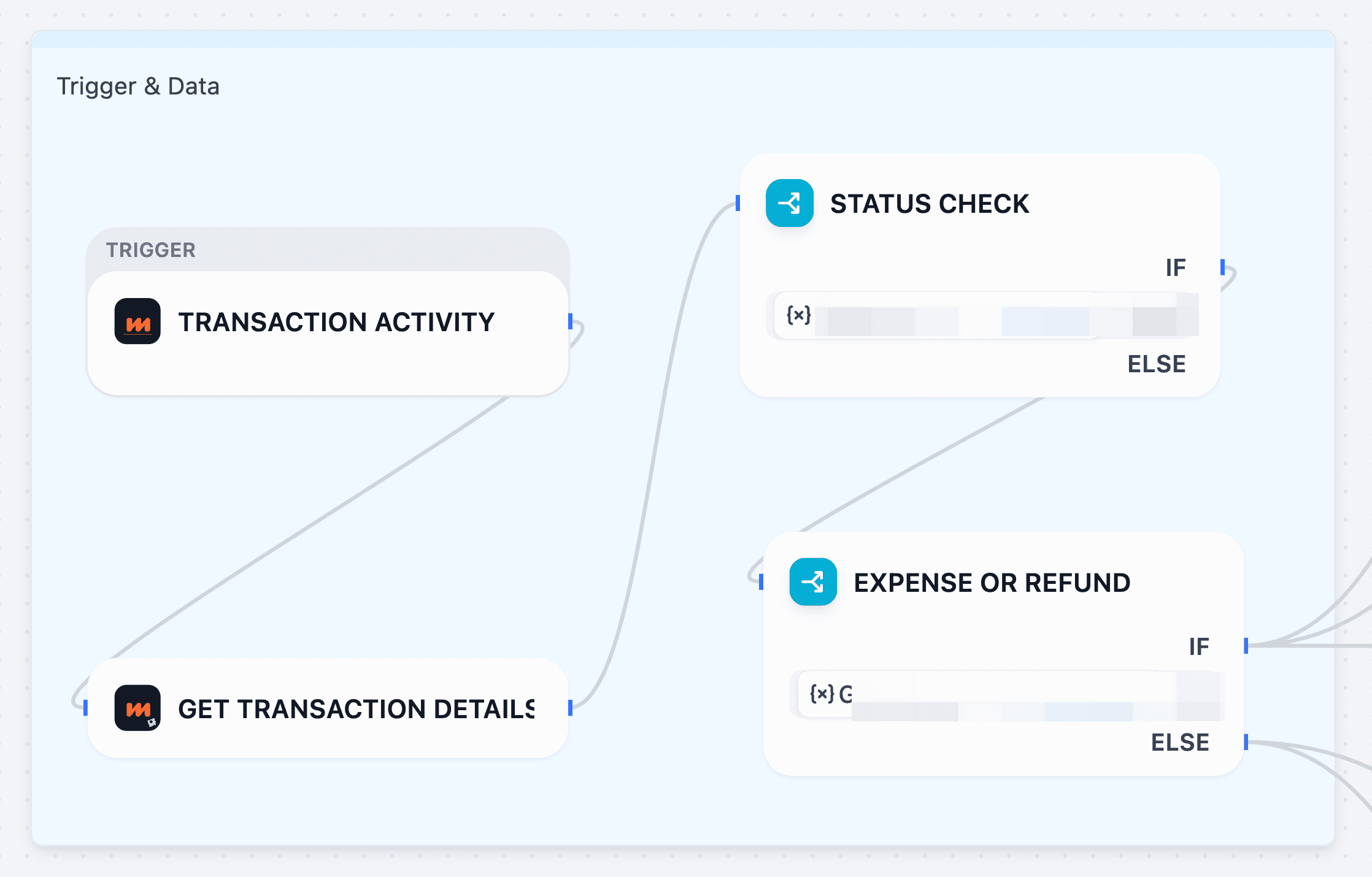

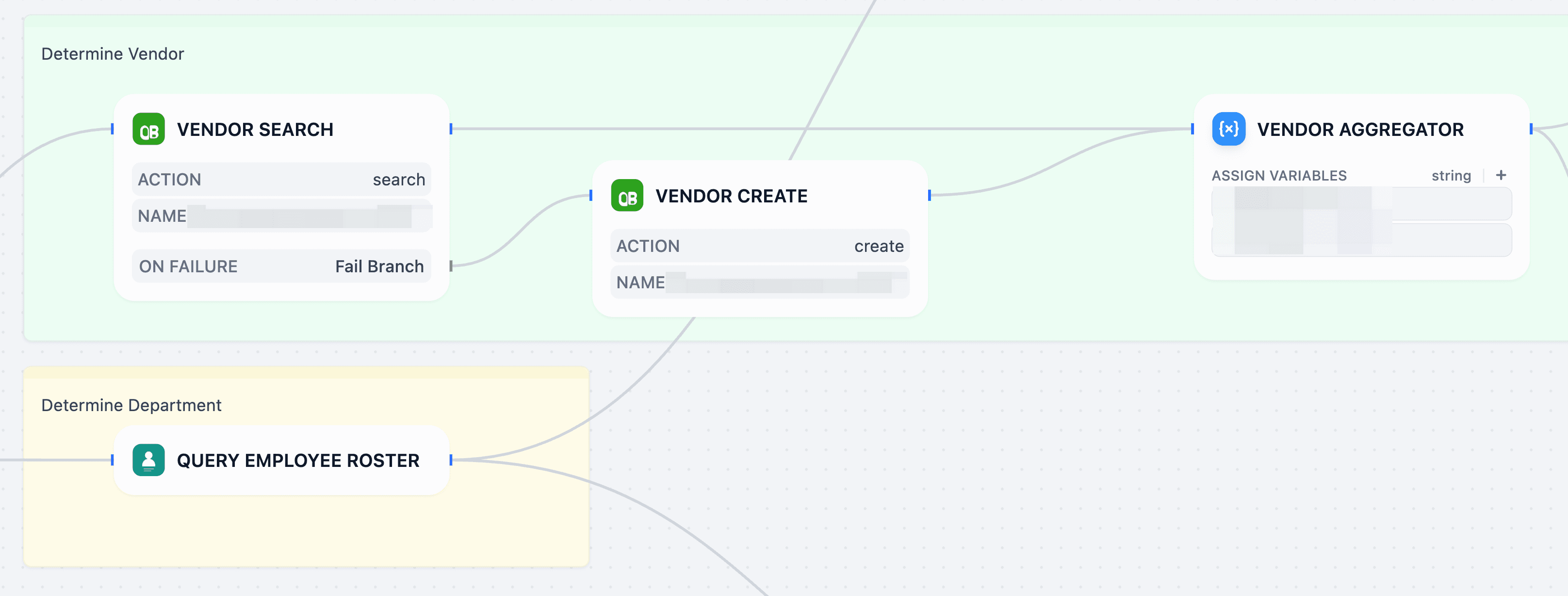

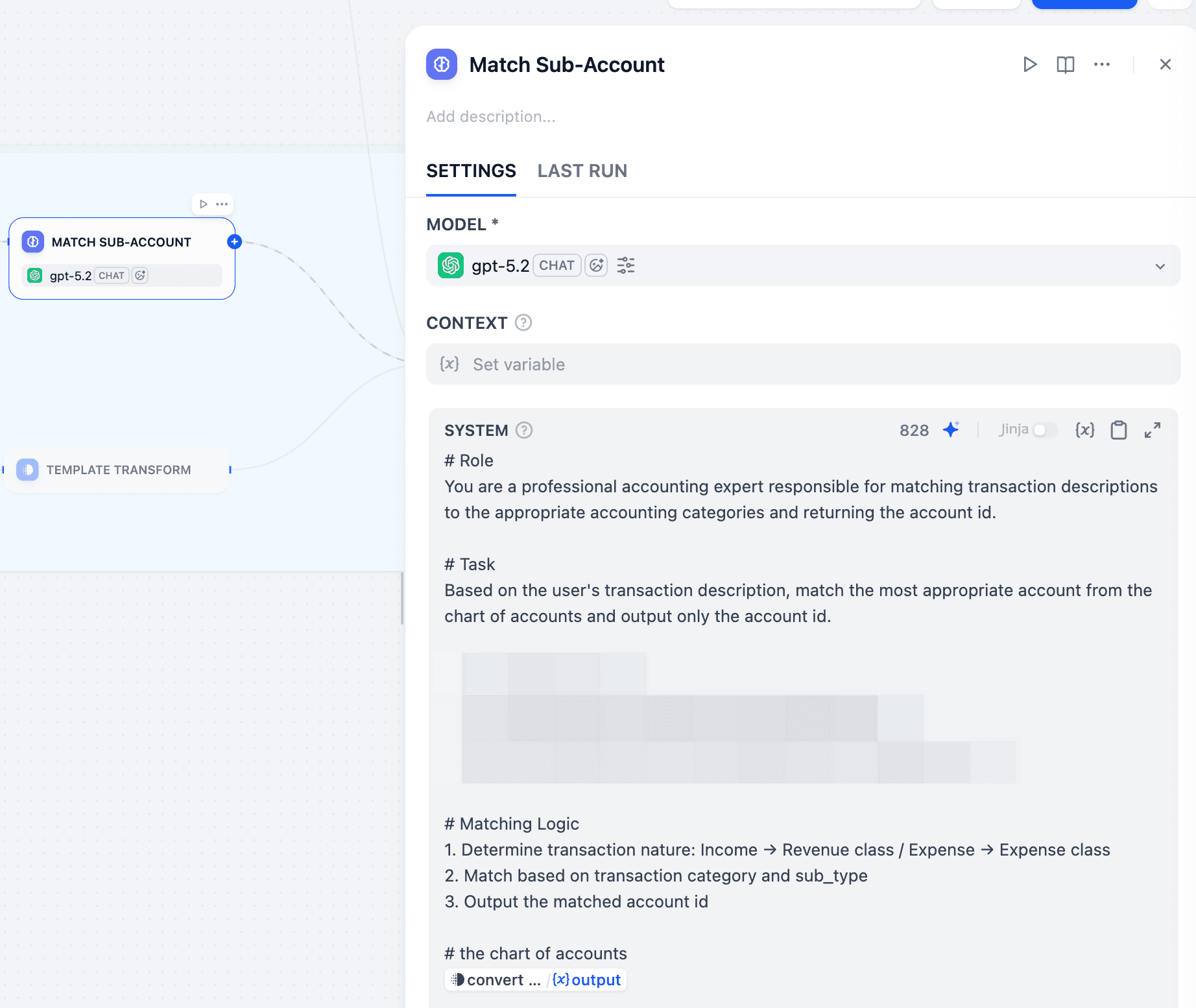

Case Study: The Automated Closed Loop from Mercury to QuickBooks

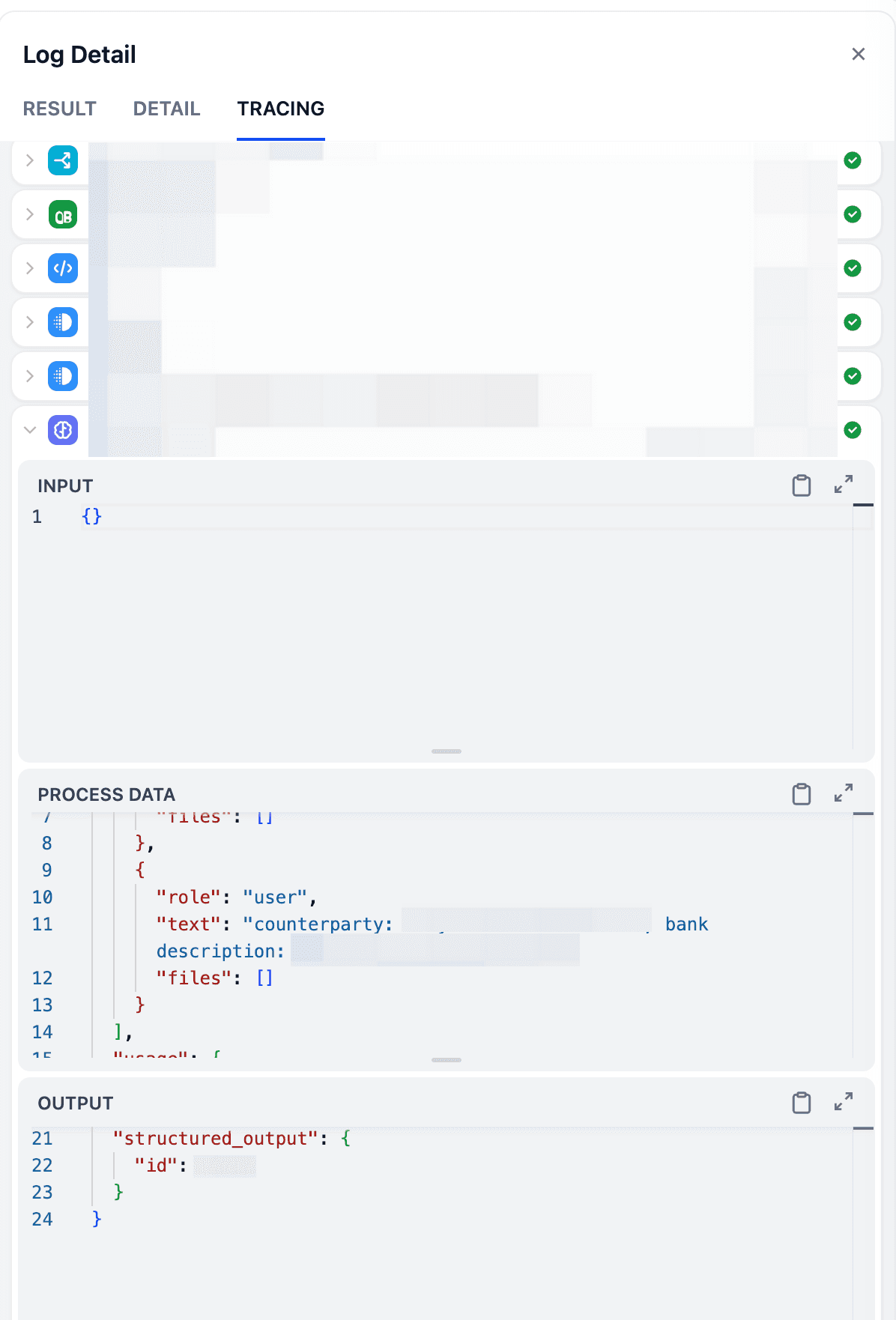

In our internal practice, we successfully built a fully automated closed loop from Mercury credit card consumption to QuickBooks bookkeeping. Here is the architectural logic of this workflow:

- Trigger & Data: When a Mercury transaction occurs, the Workflow is automatically triggered, and the system pulls complete transaction details (amount, merchant, notes, time, cardholder).

- Context Enhancement: The system automatically cleans merchant names, associates department cost centers based on cardholder information, and retrieves the supplier's historical bookkeeping habits as a reference.

- Controlled Intelligence: LLM is introduced at a fixed node in the Workflow to act as a "Finance Assistant." Based on transaction information and historical rules, it outputs two things: Account Classification Suggestions and Judgment Basis.

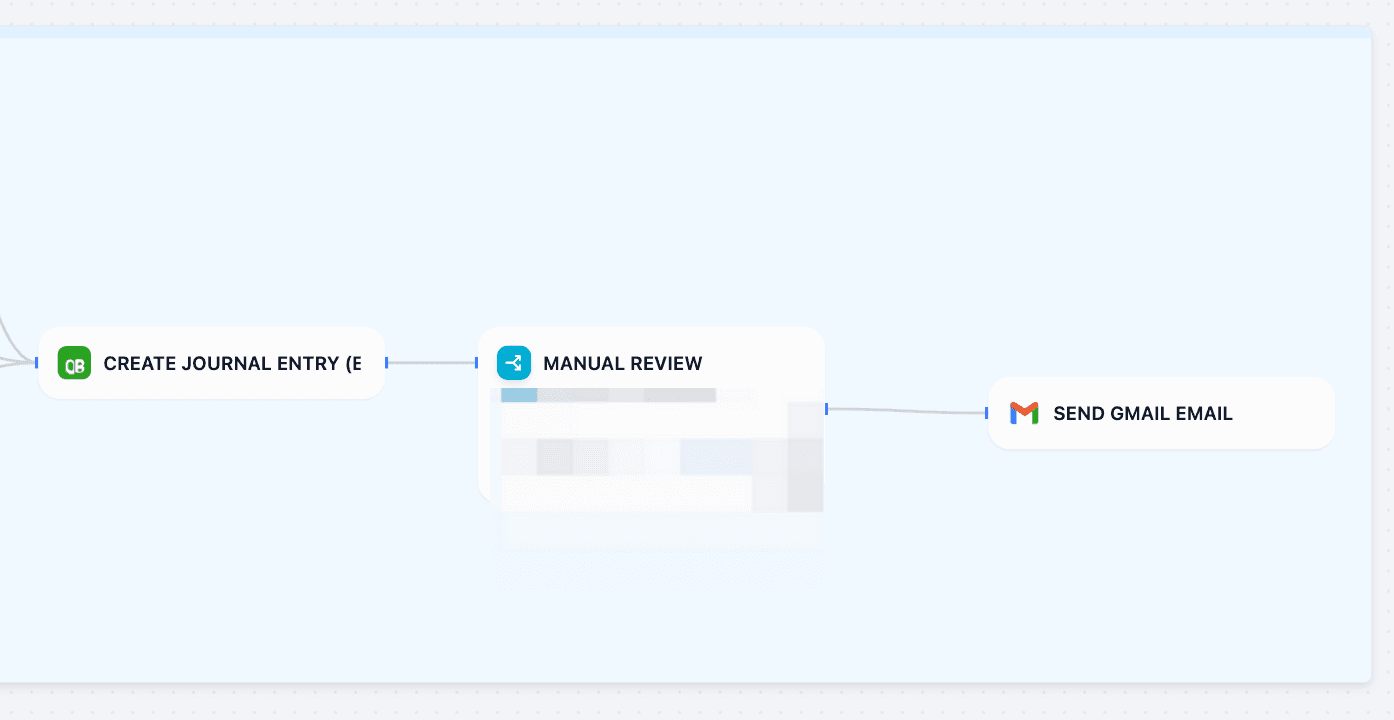

- Manual Review:

- Direct Pass Mode: For high-confidence, fixed-pattern transactions (like monthly fixed subscriptions), post directly.

- Review Mode: For new suppliers, large transactions, or sensitive accounts, the system automatically creates a "Pending" entry and emails the Finance team. Finance personnel perform a post-hoc review, ensuring the workflow remains unblocked while maintaining risk control.

- Action & Audit: Generate standard journal entries, call the QuickBooks API to write to the system, and retain full-link audit logs (Input/Output/Reasoning).

Impact Comparison:

- Processing Time Per Transaction: Dropped from 3-5 minutes to < 5 seconds.

- Human Intervention Rate: Reduced from 100% (every transaction must be seen) to ~15% (only handling exceptions).

Key Enabler: Accelerating Integration Development with Plugin Skill

For CIOs and technical teams, connecting SaaS platforms like Mercury and QuickBooks usually requires significant development effort.

In this project, we validated a new development mode—"Vibe Coding". We didn't write code from scratch but used the Dify Plugin Skill, describing interface logic in natural language to let AI assist in generating code that complies with Dify plugin specifications.

This not only greatly reduced the development threshold but, more importantly, allowed team members who understand the business but not complex engineering to participate in building the toolchain, realizing "Business-Driven Development."

👉 Click here to view how to use Dify Plugin Skill for automated plugin development

Advice for CIOs and Finance Leaders

If you are considering rolling out similar automation solutions in your organization, we suggest following these strategies:

- Reject "Black Box Automation": Do not pursue fully automatic AI processing. The core value of financial scenarios lies in being "auditable." Be sure to restrict AI to specific nodes in the Workflow as a decision support assistant, not the final decision-maker.

- Define "Error-Proof Boundaries": Which accounts must strictly match rules? Which amounts must be manually reviewed? These risk control rules must be "hard-coded" into the Workflow's conditional branches and never left to AI's free play.

- Phased Execution Roadmap:

- Phase 1 (1-2 weeks): Basic Governance. Select pilot scenarios (like SaaS subscription fees) and define the standard format for audit evidence.

- Phase 2 (3-8 weeks): Pilot Launch. Build the "Auto-Suggest + Human Review" closed loop, focusing on the exception handling process.

- Phase 3 (2-3 months): Scale Up. Assetize the accumulated rules and establish a continuous operation mechanism.

In this way, AI will no longer be an uncontrollable technological black box, but truly become a rigorous, efficient, and auditable "Digital Employee" in your finance team.

Related articles

- How to

How to Let Your Agent Call Dify Workflows Directly

Learn how to quickly invoke existing Dify apps, turning complex business workflows into a single prompt and one human approval.

Dify

Dify - How to

How to Add an AI Support Assistant to Your Website with Dify

Step-by-step tutorial on how to build, test, and embed an AI chatbot right into your website.

Dify - How to

How Marketer Builds Reliable AI Workflows

Every marketer can write a prompt. Few have figured out how to scale them. Inside: three workflows marketing teams actually build. Got a repetitive task you wish was a template? You name it. We build it for free.

Dify - How to

Get Started with Dify

In this guide, you'll learn the core fundamentals, find the right starting point for your first AI application, and grab useful resources to hit the ground running.

Dify